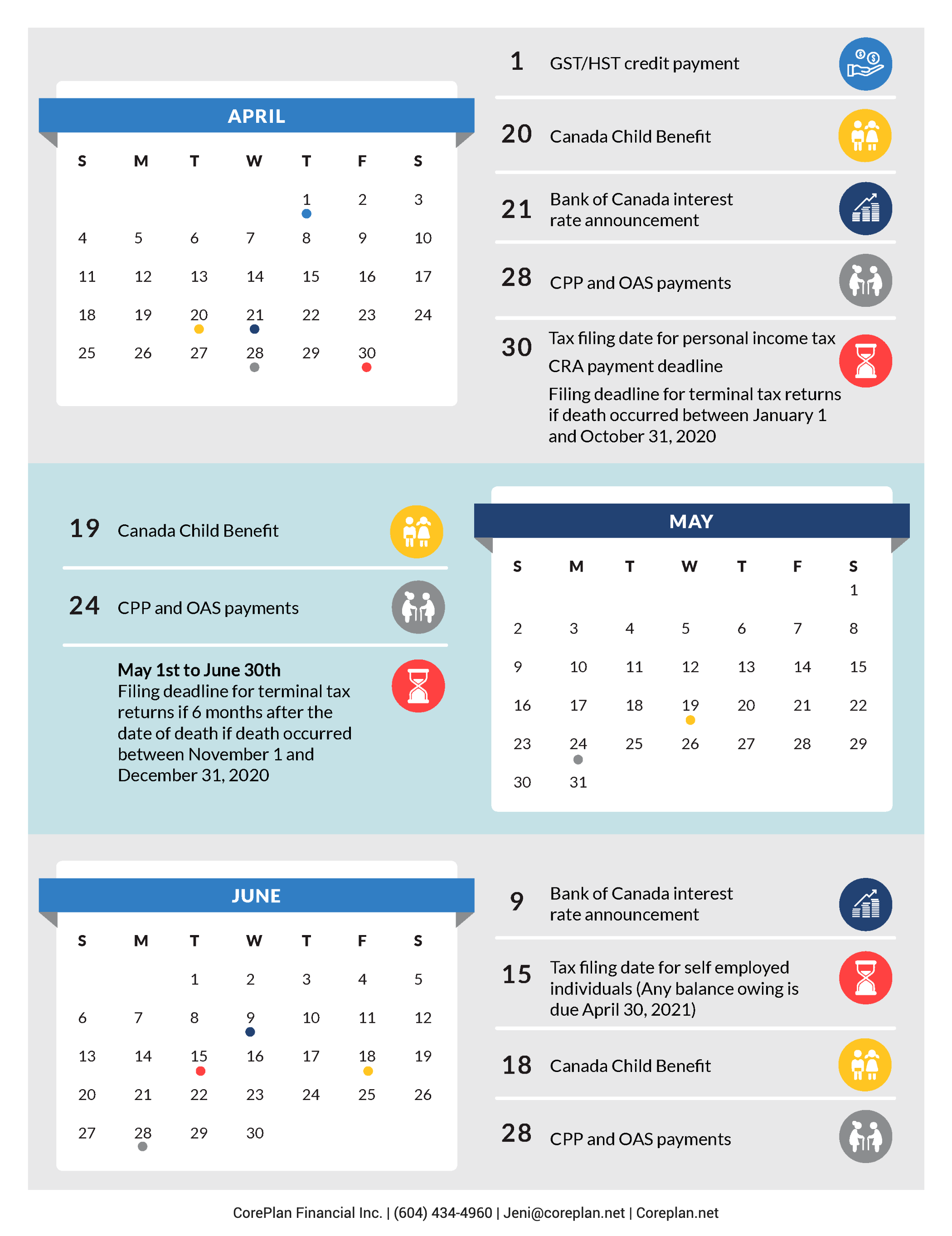

What’s new for the 2021 tax-filing season?

Tax season is upon us once again. But since 2020 was a year like no other, the 2021 tax-filing season will also be different. Both how we worked and where we worked changed for a lot of us in 2020.

Some Canadians got to work from home for the first time but saw no other disruption to their jobs. There was a much bigger disruption for other Canadians – they faced temporary or permanent job losses and had to supplement their incomes wide side gigs and emergency government programs.

The Canadian government has introduced some new tax credits and deductions in response to these changes. We’ve covered some of the highlights below.

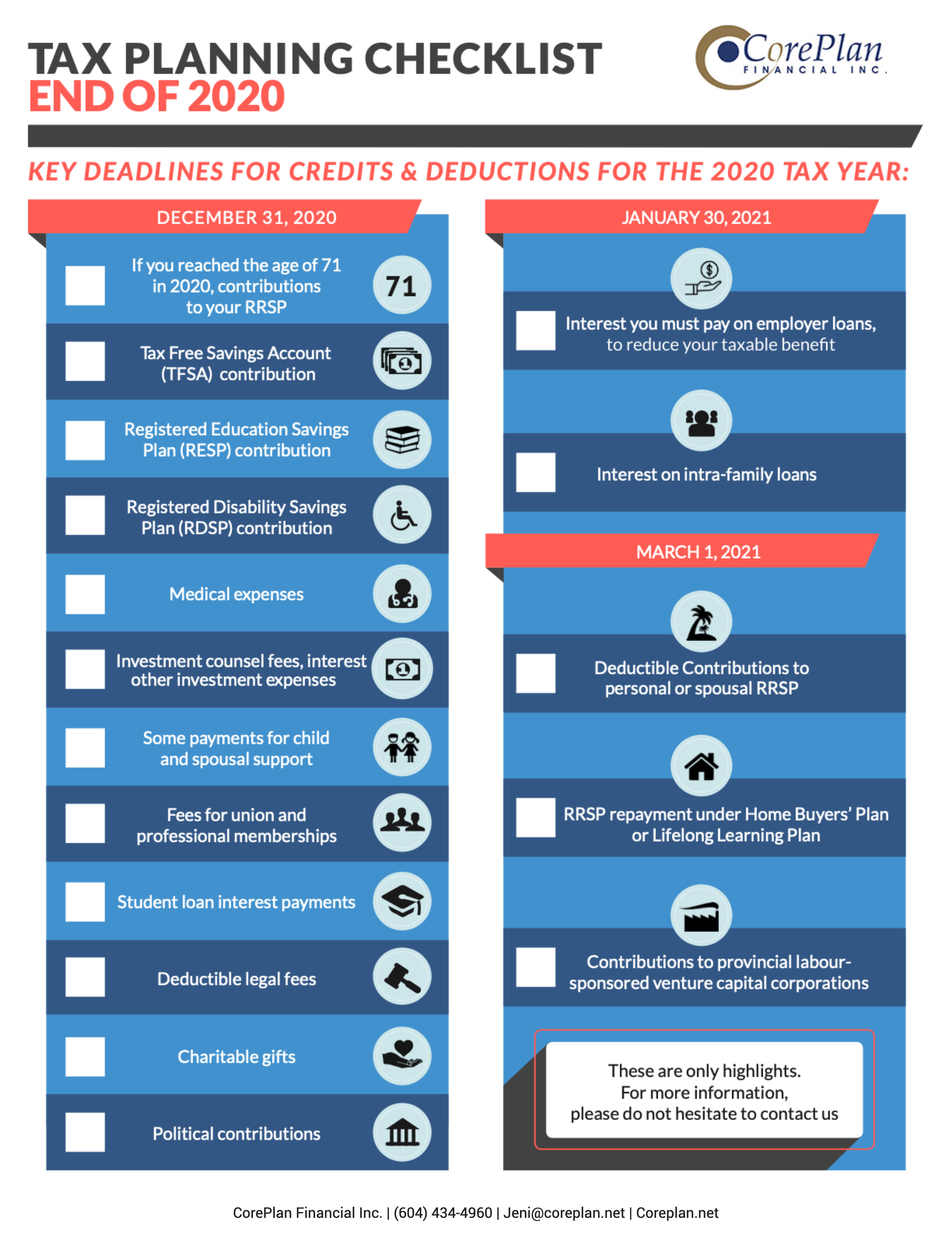

Claiming home office expenses

With a sudden shutdown happening across the country in March 2020, many Canadians stopped commuting to the office and started working from home. As a response to this, the Canada Revenue Agency (CRA) has offered a new way to claim home office expenses. If you:

-

Worked from home due to COVID-19 – for a minimum of 50 percent of the time for at least four consecutive weeks AND

-

Your employer did not reimburse you for your home office expenses.

You can claim $2 for each day – to a maximum of $400 for the year.

If you have more complicated or higher home office expenses, then your employer must provide you with a T2200 form, with a list of deductions included.

New Canada Training Credit

Suppose you are between the ages of 25 and 65 and taking courses to upgrade your skills from a college, university, or other qualifying institution. In that case, you can claim this new, refundable tax credit.

You can automatically accumulate $250 annually – and the new Canada Training Credit has a lifetime maximum of $5,000. You can claim this credit when you file your taxes.

Pandemic emergency funds

The emergency support programs helped a lot of Canadians avoid financial disaster. If you were one of the Canadians who received pandemic emergency funds, you must be aware of the tax implications.

If you received the Canada Emergency Response Benefit (CERB) or the Canada Emergency Student Benefit (CESB), no taxes were withheld at source, so you will be taxed on the full amount. If you received the Canada Recovery Benefit (CRB), Canada Recovery Sickness Benefit (CRSB), or Canada Recovery Caregiver Benefit (CRCB), the CRA withheld a 10% tax at source, so you may not owe additional taxes on this income.

New digital news subscription tax credit

This is a new, non-refundable tax credit that is calculated at 15 percent – and is eligible for up to a maximum of $500 in qualifying subscription expenses. To qualify for this credit, you must subscribe to one or more qualified Canadian journalism organizations – and you could save up to $75 a year thanks to this credit.

I’m here to help you understand where you owe taxes and how you can lower your tax bill. Give me a call today!