¹The amount and tax rate will vary based on province/territory you live in.

It’s worth considering ensuring that you receive a salary high enough to take full advantage of the maximum RRSP annual contribution that you can make. For 2020, salaries of $154,611 will provide the maximum RRSP room of $27,830 for 2021.

Is it worth accruing your salary or bonus this year?

You could consider accruing your salary or bonus in the current year but delaying payment of it until the following year. If your company’s year-end is December 31, your corporation will benefit from a deduction for the year 2020. The source deductions are not required to be remitted until actual salary or bonus payment in 2021.

Stock Option Plan

If your compensation includes stock options, check if you will be affected by the stock option rules that went into effect on January 1, 2020. These new rules cap the amount of specific employee stock options eligible for the stock option deduction at $200,000 as of January 1, 2020. These rules will not affect you if a Canadian controlled private corporation grants your stock options.

Tax-Free Amounts

If you own your corporation, pay yourself tax-free amounts if you can. Here are some ways to do so:

-

Pay yourself rent if the company occupies space in your home.

-

Pay yourself capital dividends if your company has a balance in its capital dividend account.

-

Return “paid-up capital” that you have invested in your company

Do you employ members of your family?

Employing and paying a salary to family members who work for your incorporated business is worth considering. You could receive a tax deduction against the salary you pay them, providing that the salary is “reasonable” with the work done. In 2020, the individual can earn up to $13,229 (increased for 2020 from $12,298) and pay no federal tax. This also provides the individual with RRSP contribution room, CPP and allows for child-care deductions. Bear in mind there are additional costs incurred when employing someone, such as payroll taxes and contributions to CPP.

COVID-19 wage subsidy measures for employers

To deal with the financial hardships introduced by COVID-19, the federal government introduced two wage subsidy measures:

-

The Canada Emergency Wage Subsidy (CEWS) program. With this, you can receive a subsidy of up to 85% of eligible remuneration that you paid between March 15 and December 19, 2020, if you had a decrease in revenue over this period. You must submit your application for the CEWS no later than January 31, 2021.

-

The Temporary Wage Subsidy (TWS) program. With this program, which reduces the amount of payroll deductions you needed to remit to the CRA, you can qualify for a subsidy equal to 10% of any remuneration that you paid between March 18, 2020, and June 19, 2020. You can claim up to a maximum of $1,375 per employee and $25,000 in total.

You can apply for both programs if you are eligible. If you qualify for the TWS but did not reduce your payroll remittances, you can still apply. The CRA will then either pay the subsidy amount to you or transfer it over to your next year’s remittance.

Business Tax

Claiming the Small Business Deduction

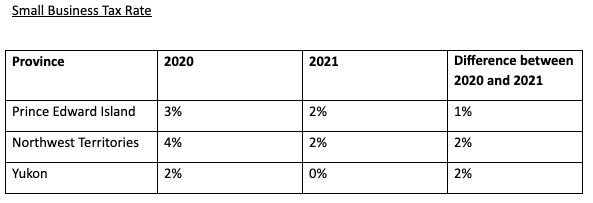

Are you able to claim a small business deduction? The federal small business tax rate decreased to 9% in 2019. It did not increase in 2020, nor is it expected to increase in 2021. From a provincial level, there will be changes in the following provinces: